Bond Yields May Eye Higher Ground After Soft Jobs Data, Treasury Borrowing Surge

The job report on Friday delivered a big downside surprise with just 12k jobs created in October. Certainly nowhere near my model’s estimates, but then again, given the size of revisions over the past few months, who knows?

Between seasonal adjustments and the birth/death model, anything is possible. These reports seem to be a joke at this point.

The household survey appears to be more reliable, and while that number was down, overall it has been steady for some time, which is probably good enough.

In the meantime, the unemployment rate came in at 4.145324%, highlighting how close it was to reaching to 4.2% during the month.

Imagine what might have happened if, instead of 428,000 people leaving the labor force in October, only 400,000 had exited.

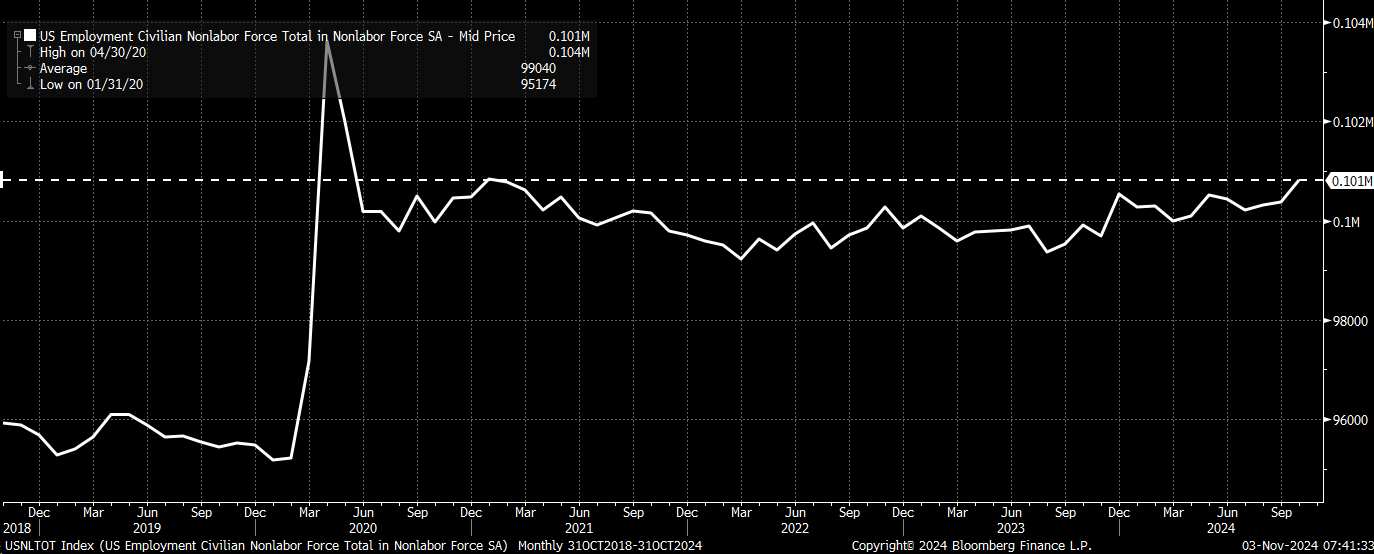

The unemployed workers could have risen just enough to push that number from 4.1% to 4.2%. Meanwhile, the number of people not in the labor force increased to about 101 million, its highest level since February 2021.

Add some people here, take some people from there, sprinkle in mild birth/death adjustments, and top it off with a touch of seasonality, and presto—you have a job report that’s not too hot, not too cold, but just right.

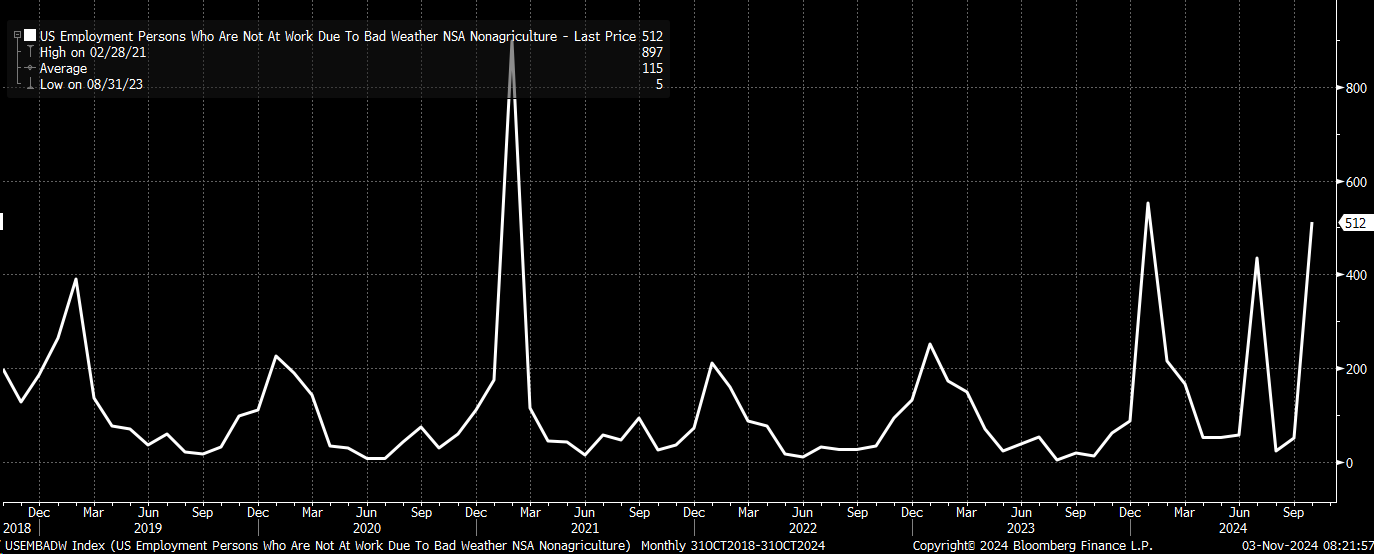

But clearly, the bond market saw right through it. Looking at the data, it’s evident that next month, many who didn’t work due to bad weather will likely return to the labor force in November. The real question is how many there were, as these figures are only reported on a non-seasonally adjusted basis, but stood at 512,000.

Whatever the case, the bond market seemed to view these numbers as much better than they appeared on the surface, as the 10-year rate rose ten bps on Friday alone, closing at 4.38%. This move cleared the significant resistance level at 4.33% and now faces a downtrend at around 4.4%, which I believe will break through.

And why shouldn’t it, when at the low-key Treasury Quarterly Refunding Announcement, it was revealed that the Treasury will need to borrow, get this, $823 billion in the January–March 2025 quarter. I’d seen many estimates around the $700 billion mark, so this was a much larger-than-expected increase.

In addition, based on the latest jobs data, wage growth appears to be sticky at 4%, a rate that isn’t consistent with 2% inflation. Plus, when you annualize the wage data at a 3-month annualized rate, it’s accelerated to 4.5%.

Trump Re-Election

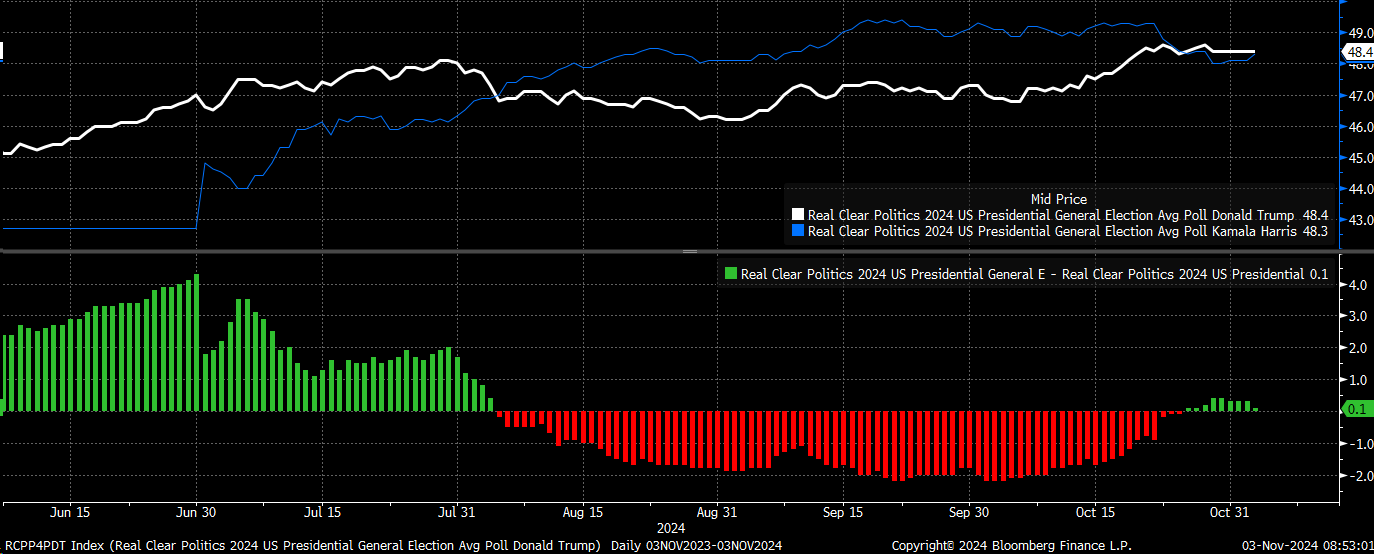

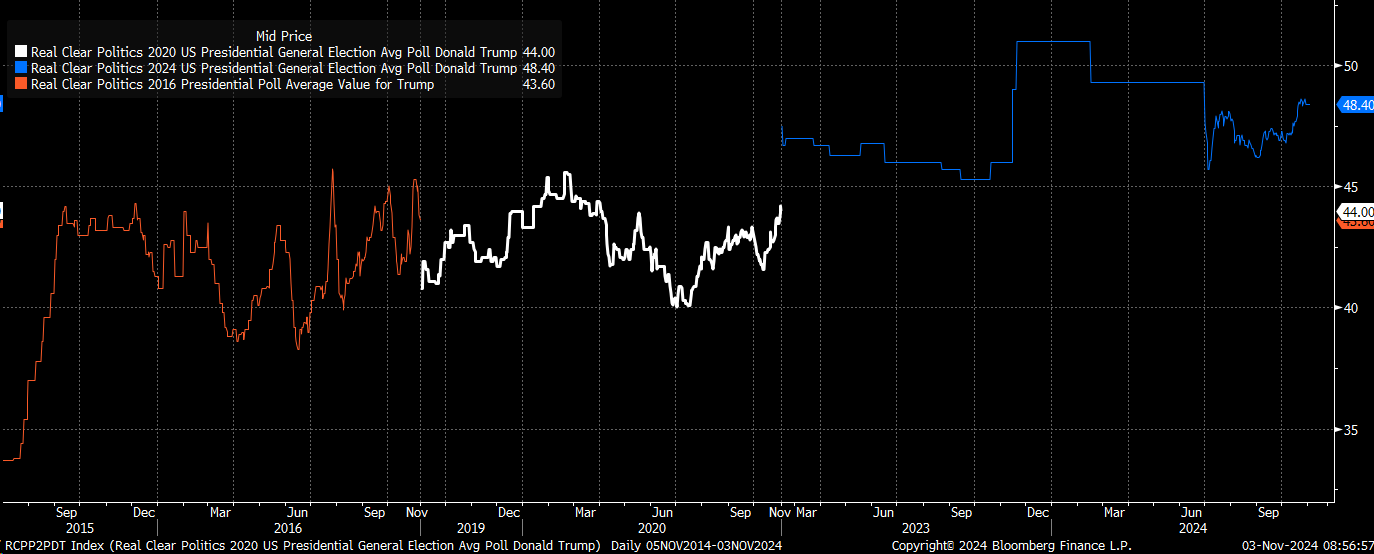

Regarding Tuesday’s election, I will go out on a limb and predict that Trump will win by a wide margin. Currently, he’s leading in the RealClearPolitics average by 0.1%. In comparison, in 2020, Biden was ahead by 7.2%, and in 2016 Clinton led by 1.8%.

So, for the first time, Trump is not the underdog. He clearly has momentum on his side as well.

He is also beating himself compared to 2016 and 2020, when he polled at 43.6 and 44%, respectively.

He is also polling better in swing states like Pennsylvania, Michigan, Georgia, and Arizona versus 2020.

When you look at these numbers and see that Trump is up by four percentage points compared to himself in the two prior elections and is beating himself in five battleground states, it seems to me that he should be able to win by a comfortable margin. This may not be what some people want to hear, but it’s what the data shows. We can interpret this data much like we analyze economic indicators or earnings reports. I guess we will find out the results on Tuesday night.

I get the feeling he will end up with 312 Electoral votes.

Anyway,

Original Post