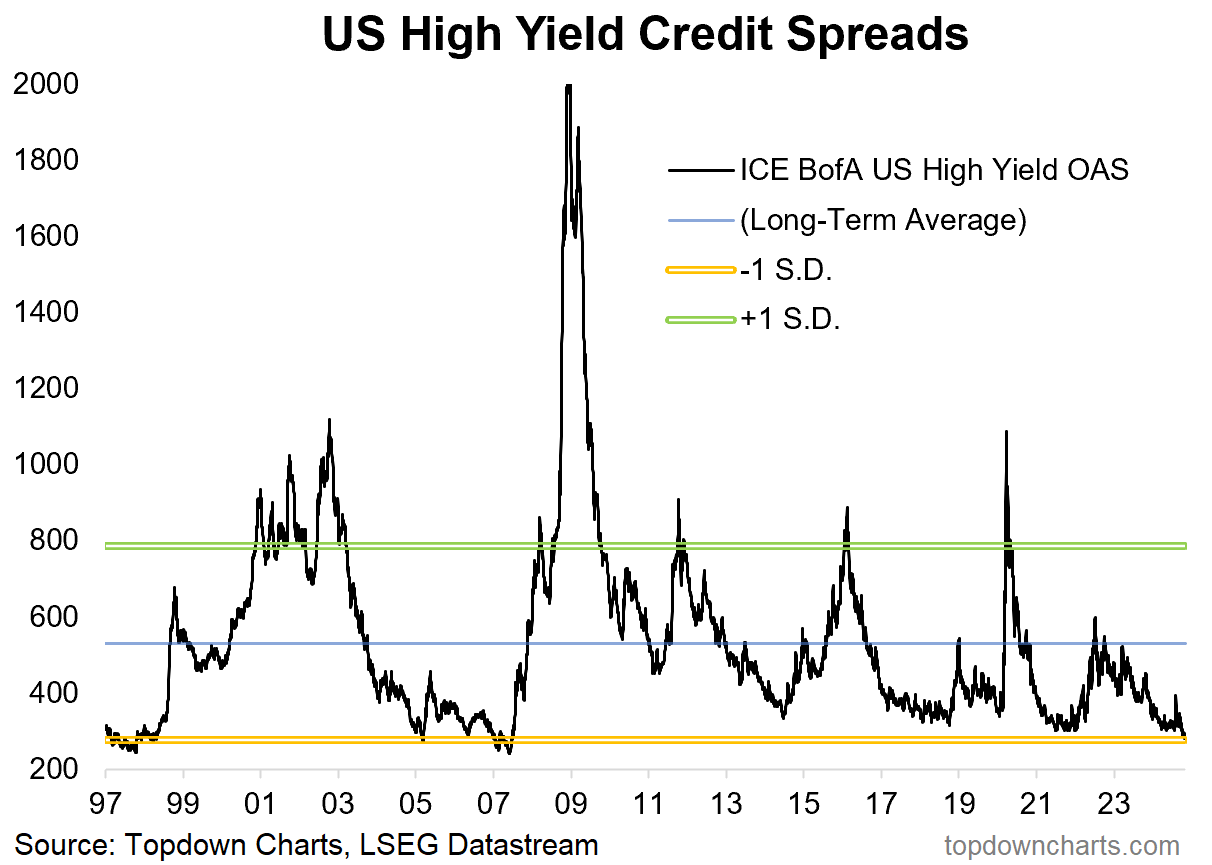

Credit Spreads at 17-Year Lows Reflect Confidence But Signal Growing Risk

Credit spreads have narrowed down to the lowest point since the pre-financial crisis period. It echoes the strength in the Stock market (and expensive valuations), and paradoxically is both: 1. a sign of strength; and 2. a risk to plan for:

- First, the good: credit spreads fall when risk sentiment is bullish, the economy is strong, financial conditions are easy, the stock market is rising, and most of all — credit risk is low (at least, current/trailing credit risk).

- But also, the bad: credit spreads are basically a contrarian indicator, low levels mean “expensive valuations” (mirroring the stockmarket PE ratios), often indicating complacency and overall lower compensation for taking on credit risk.

On that note, what do we even mean by “credit spreads“?

Credit spreads are the difference between the interest rate (yield) on corporate bonds vs the risk-free rate (i.e. maturity-matched treasury bond yield). The credit spread therefore is the risk premium that investors are paid over and above the risk-free rate for taking on credit risk.

The trade-off is to earn a bit higher interest by investing in corporate bonds instead of treasuries but take on the risk of default (and some level of credit loss).

Credit risk can be mitigated by investing in higher grade issues (better credit quality), diversification (holding so many bonds that 1 or 2 defaults won’t wipe out your returns or capital), and active management (e.g. decreasing exposure to credit risk or buying protection when forward-looking risk is high).

On that last note, the chart below is most relevant to active fixed-income investors and asset allocators because historically the best time to take on credit risk i.e. the time when you get richly compensated, is when credit spreads spike to very high levels.

Meanwhile, the worst time is typically when credit spreads reach rock bottom.

Much like when the stock market reaches expensive levels, it’s the time when everyone chases the prospect of higher returns and throws caution to the wind — and it’s also usually the time to move more defensive.

The point where confidence becomes complacency is when the business cycle starts to deteriorate, credit risk rises, and credit spreads become unjustifiably low.

I don’t think we’re quite there yet as there is still some resilience in the economic data, but this is the point of maximum required vigilance — echoing my observations elsewhere that stocks are also looking increasingly expensive, and forward-looking risk therefore is on the rise more broadly.

Key point: The 17-year low in credit spreads represents bullish confidence and strong economic conditions, but also implores increased vigilance for active fixed-income investors and asset allocators.

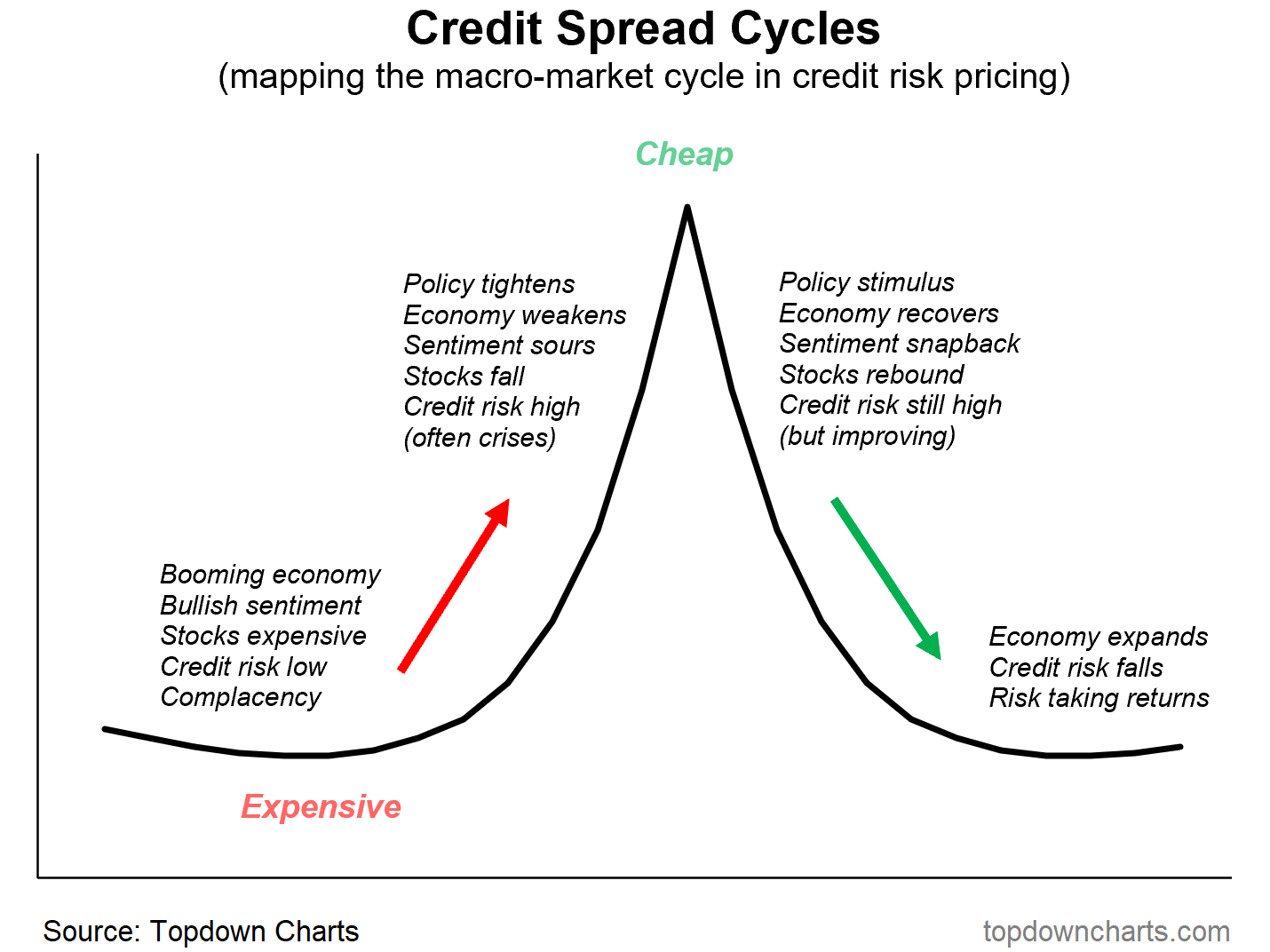

Concepts Section: Credit Spread Cycles?

While I touched upon the cycle/concept of navigating credit spreads above, I thought it might be useful to show a credit spread version of the typical stockmarket cycle from this article.

Credit spreads go through cycles, just like the stock market (but inverted) — they reach the lows during times of economic expansion and boom, and start to increase later in the cycle as policy tightens and investors grow wary of previous excess risk-taking.

And then at some stage, a breakpoint is reached where the data deteriorates, defaults begin to rise, and often times some sort of crisis or credit event unfolds and credit spreads blow out to very high levels.

Eventually, they reach a peak, often precipitated by some sort of intervention or stimulus announcements to ring-fence the crisis and/or trigger a recovery in confidence, sentiment, and the economy.

Markets then rebound, sentiment improves, and the economy recovers—credit risk may still be somewhat elevated as marginal borrowers struggle to make payments, but is on an improving path.

And then finally the thing comes full circle where confidence turns to complacency, caution gives way to risk-taking, and credit risk premiums evaporate once again.

Original Post